New York, NY, August 15, 2023 – (BUSINESS WIRE) – As previously announced, in connection with the Agreement and Plan of Merger, dated as of July 28, 2022 the “Merger Agreement”, by and among JetBlue Airways Corporation (NASDAQ: JBLU), Sundown Acquisition Corp., and Spirit Airlines, Inc. (NYSE: SAVE), JetBlue has set August 25, 2023, as the record date for the August 2023 prepayment to Spirit stockholders of $0.10 per Spirit share (the “August 2023 Additional Prepayment”), with payment of the August 2023 Additional Prepayment to occur on August 31, 2023. Pursuant to the Merger Agreement, Spirit stockholders as of the August 25, 2023, record date will be entitled to receive the August 2023 Additional Prepayment.

CALGARY, Alberta & KANSAS CITY, Mo.–(BUSINESS WIRE)– Canadian Pacific Railway Limited (NYSE: CP) and Kansas City Southern (NYSE: KSU) have announced they have jointly filed a railroad control application with the Surface Transportation Board (“STB”) regarding the proposed transaction to create Canadian Pacific Kansas City (“CPKC”), the only single-line railroad linking the United States, Mexico and Canada.

The comprehensive control application provides an overview of the proposed operational integration of the CP and KCS rail networks, the impact of that consolidation on the companies’ finances and labour needs, and the anticipated competitive and other benefits that will flow from providing shippers with new and better transportation alternatives. Information in the filing outlines the public and customer benefits a CP-KCS combination would bring, including more efficient north-south trade arteries to support the interconnected supply chains of the United States, Mexico and Canada.

In addition to the central foundation of the transaction to invigorate transportation competition and support economic growth across North America, the CP-KCS combination will generate many other public benefits, including:

The creation of more than 1,000 direct new jobs system-wide, including approximately 760 in the United States, over the next three years brought about by expanded rail operations across the combined network.

Capital investments in new infrastructure of more than USD$275 million1 over the next three years to improve rail safety and capacity of the core north-south CPKC main line between Louisiana and the Upper Midwest.

Avoidance of more than 1.5 million tons of greenhouse gas (GHG) emissions within five years due to the improved efficiency of CPKC versus current operations.

Diverting 64,000 long-haul truck shipments to rail annually with new CPKC intermodal services, eliminating another 1.3 million tons of GHG emissions over the next two decades, saving $750 million in highway maintenance costs.

Rail customers will not experience a reduction in independent railroad choices as a result of the CP-KCS combination. The joint control application reiterates the applicants’ commitment to keep all existing freight rail gateways open on commercially reasonable terms, including the Laredo gateway between the United States and Mexico, and shows how customers will not lose competitive routings because no new regulatory “bottlenecks” are being created. It also describes how the combined company will compete aggressively to attract traffic to its network via new single-line lanes between Canada, the Upper Midwest and the Gulf Coast, Texas, and Mexico.

More than 960 stakeholders, including more than 440 shippers, 186 smaller railroads, dozens of public officials, eight major ports, railroad labor unions representing both CP and KCS employees and 289 rail industry suppliers have written letters to the STB supporting CP’s proposed combination with KCS.

CP has agreed to acquire KCS in a stock and cash transaction representing an enterprise value of approximately $31 billion, which includes the assumption of $3.8 billion of outstanding KCS debt. The transaction, which has the unanimous support of both boards of directors, values KCS at $300 per share, representing a 34 percent premium, based on the CP closing price on Aug. 9, 2021, the date prior to which CP submitted a revised offer to acquire KCS, and KCS’ unaffected closing price on March 19, 2021.2

The transaction is subject to approval by shareholders of each company along with satisfaction of customary closing conditions, including Mexican regulatory approvals. Shareholders are expected to vote on the transaction later this year.

CP’s ultimate acquisition of control of KCS’ U.S. railways is subject to the approval of the STB. In April 2021, the STB determined it would review the CP-KCS combination under the merger rules in existence prior to 2001 and the waiver granted to KCS in 2001 to exempt it from the 2001 merger rules. In August 2021, the STB reaffirmed that the pre-2001 rules would govern its review of the CP-KCS transaction. On Sept. 30, 2021, the STB confirmed that it has approved the use of a voting trust for the CP-KCS combination.

The STB review of CP’s proposed control of KCS is expected to be completed in the second half of 2022. Upon obtaining control approval, the two companies will be integrated fully over the ensuing three years, unlocking the benefits of the combination.

While remaining the smallest of six U.S. Class 1 railroads by revenue, the combined company would have a much larger and more competitive network, operating approximately 20,000 miles of rail, employing close to 20,000 people, and generating total revenues of approximately $8.7 billion based on 2020 actual revenues.

For more information about the benefits of the CP-KCS combination, visit futureforfreight.com

AirAsia Group Berhad (Kuala Lumpur: 5099.KL) is pleased to announce that Dr. Stanley Choi Chiu Fai has joined the Group as a substantial shareholder via his wholly-owned entity Positive Boom Ltd. on 18 February 2021. He acquired 167.1 million AirAsia shares in the first tranche of the private placement, raising his shareholding in the group to 332.5 million shares equating to a 8.96% stake.

Dr. Stanley Choi is the Chairman of Head & Shoulders Financial Group, as well as the Chairman and Executive Director of International Entertainment Corporation (IEC), a company listed on the main board of Hong Kong Stock Exchange (1009.HK). He is also the only co-founding member from Hong Kong for YunFeng Capital – a private equity fund started in 2010 by a group of successful entrepreneurs and influential industry leaders, named after its co-founder Jack Ma Yun, founder of Alibaba Group, and David Yu Feng, founder of Target Media.

His previous directorships include his appointment as Executive Director of Target Insurance (Holdings) Limited (stock code: 6161.HK) from 2014 to 2019, Director of ZhongAn Online P&C Insurance Co. Limited (stock code: 6060.HK) from 2013 to 2016 and Executive Director of Media Asia Group Holdings Limited (stock code: 8075.HK) from 2011 to 2015.

The successful businessman possesses more than 20 years of experience in financial services and merger & acquisition transactions, with a particular focus on private equity investment. He was a seed investor of Kidswant, a Chinese-startup that has now become a leading maternity, baby and children’s product retailer in China with a valuation of over USD3 billion.

Dr Stanley Choi, Chairman of Head & Shoulders Financial Group said: “It is my great pleasure and honour to gain a substantial ownership stake in AirAsia Group – the world’s best low cost airline and one of Asia’s biggest known brands that has successfully pivoted into digital business as well. I believe the worst period in the aviation industry’s history has now passed. I am confident that air travel will bounce back and that under Tan Sri Tony’s and Datuk Kamarudin’s leadership, and with vaccines being rolled out across the region and globally, AirAsia has a very bright future ahead. I look forward to working with everyone at AirAsia.”

Datuk Kamarudin Meranun, Executive Chairman of AirAsia Group said: “We are thrilled to welcome Dr Stanley Choi as a strategic shareholder of AirAsia Group, bringing an impressive track record and solid reputation as a business powerhouse to our Group. We are confident that he will add value to our digital business development in China through his vast experience and network with top digital players in the country.

Dr Stanley Choi graduated with a Master’s Degree of Science from the University of Illinois at Urbana Champaign, United States in 1996. In 2013, he obtained a Doctoral Degree of Business Administration from the City University of Hong Kong.

BRUSSELS (Reuters) – The European Union’s competition watchdog on Monday approved French state aid worth 7 billion euros ($7.66 billion) for Air France <AF.PA>, saying the support would provide cash to soften the economic shock of the coronavirus pandemic.

Airlines across Europe have sought state rescues as coronavirus lockdowns have forced them to ground their fleets for more than a month, with no end in sight.

“This 7 billion euro French guarantee and shareholder loan will provide Air France with the liquidity that it urgently needs to withstand the impact of the coronavirus outbreak,” the EU’s top competition official Margrethe Vestager said in a statement.

The European Commission noted the importance of Air France, with more than 300 planes, to the French economy and the role it has played in repatriating stranded citizens and transporting medical supplies.

The Commission said in its statement that the support will take the form of a state guarantee on loans and a subordinated shareholder loan to the company by the French state.

The French and Dutch governments each hold close to 14% of the Air France-KLM group, which was created by the 2004 merger between the two national carriers.

(Reporting by Gabriela Baczynska and Robin Emmott, editing by Ed Osmond and Barbara Lewis)

FILE PHOTO: Air France airplanes on the tarmac at Paris Charles de Gaulle airport in Roissy-en-France

(Reuters) – Boeing Co suppliers Hexcel Corp and Woodward Inc on Monday called off their planned all-stock merger as widespread travel bans to curb the coronavirus pummels demand in the aerospace sector.

The companies, which make and supply aircraft parts, had agreed to a merger in January in a $6.4 billion deal.

“Although we are disappointed with this outcome, we are confident this is the right decision for our customers, our shareholders, and our employees,” the companies said in a joint statement.

The market rout triggered by the coronavirus pandemic and the resulting economic downturn has thrown a wrench into corporate deal making. Last month U.S. printer maker Xerox Holdings Corp walked away from its $35 billion hostile cash-and-stock bid for HP Inc.

Boeing, which halted the production of its grounded 737 MAX aircraft in January, said on Sunday it would extend the suspension of production at its Washington state facilities until further notice.

Boeing is Hexcel’s second-biggest customer, accounting for a quarter of the company’s annual sales. Hexcel also supplies Airbus SE.

Woodward gets about 15% of its annual sales from Boeing, its biggest customer.

(Reporting by Ankit Ajmera in Bengaluru; Editing by Shounak Dasgupta and Devika Syamnath)

Consortium of bidders led by Advent, Cinven and RAG foundation

Sales proceeds pave the way for further transformation of thyssenkrupp

Cash inflow remains within the company

Buyers give far-reaching site and employment guarantees for tk Elevator

Closing and purchase price payment expected by the end of the current fiscal year

Martina Merz: “With the sale of Elevator, thyssenkrupp can pick up speed again. We will reduce the company’s debt as far as is necessary and at the same time invest as much as is reasonable in its further development.”

thyssenkrupp sells its Elevator Technology business entirely to a consortium led by Advent, Cinven and RAG foundation. The respective Executive Board decision was approved on Thursday evening by the Supervisory Board of thyssenkrupp AG. The purchase agreement has been signed. Closing of the transaction is expected by the end of the current fiscal year. The purchase price is €17.2 billion. thyssenkrupp will reinvest part of the purchase price[1] (€1.25 billion) in a stake in the elevator business. The transaction is subject to merger control approvals, although thyssenkrupp does not expect the competent authorities to have any reservations. The proceeds from the transaction will remain within the company and are to be used to the extent necessary to strengthen the balance sheet. Alongside this, the proceeds shall be used to advance the development of the remaining businesses and the portfolio. As announced at the Annual General Meeting at the end of January, thyssenkrupp is proceeding the analysis phase so that a decision on the concrete use of funds can be taken in May.

Martina Merz, CEO of thyssenkrupp AG: “With the sale, we are paving the way for thyssenkrupp to become successful. Not only have we obtained a very good selling price, we will also be able to complete the transaction quickly. It is now crucial for us to find the best possible balance for the use of the funds. We will reduce thyssenkrupp’s debt as far as is necessary and at the same time invest as much as is reasonable in developing the company. With this, thyssenkrupp can pick up speed again.”

The sale of Elevator is a favorable solution not only for the company, its shareholders, customers and employees, but also for the elevator business itself. In the consortium, thyssenkrupp has found new owners for the elevator business who have extensive industrial expertise and offer the workforce a high degree of security. The buyers have a strong track record in profitably growing and nurturing companies to become global champions.

In negotiations with employee representatives and the IG Metall trade union, the buyers have committed to far-reaching site and employment guarantees. In addition, it was agreed that the buyers will continue to manage thyssenkrupp Elevator as a global group. The company will also remain based in Germany and employee co-determination will continue. That means the solution is in line with thyssenkrupp’s understanding of corporate and social responsibility.

“We are not pleased to part with our employees and the elevator business. Nevertheless, today is a good day for everyone involved. With this step, we are opening up real prospects for the future: for the elevator business as an independent company and, with the financial solidity we have gained, also for all other areas of thyssenkrupp,” Martina Merz added.

New Technology Creates Hyper Elevators That Can Go Sideways

MILAN (Reuters) – Italian tax authorities believe that Fiat Chrysler Automobiles <FCAU> underestimated the value of its U.S. business by 5.1 billion euros following Fiat’s phased acquisition of Chrysler, according to a company filing and a source close to the matter.

The audit, which concerns transactions dating back to 2014, could result in FCA having to pay back taxes for $1.5 billion, the source added, confirming a report by Bloomberg.

FCA said in its third-quarter report that the tax authorities had issued to the company a final audit report in October this year “which, if confirmed in the final audit assessment, could result in a material proposed tax adjustment related to the October 12, 2014 merger of Fiat SpA into FCA NV.”

It said the issuance of a final audit report starts a 60-day negotiation period, which ends with the issuance of a final audit assessment expected to be received by the end of December 2019.

“The company believes that its tax position with respect to the merger is fully supported by both the facts and applicable tax law and will vigorously defend its position,” it said in the third-quarter report.

A spokesman for Italy’s tax agency declined to comment.

“At this time, we cannot predict whether any settlement may be reached or if no settlement is reached, the outcome of any litigation. As such, we are unable to reliably evaluate the likelihood that a loss will be incurred or estimate a range of possible loss,” Fiat said.

News of the tax probe comes at a delicate time for Fiat Chrysler, which is finalizing talks with PSA, the maker of Peugeot and Citroen, over a planned $50 billion merger to create the world’s fourth-largest automaker.

(Reporting by Silvia Aloisi in Milan; Editing by Anil D’Silva)

DETROIT (Reuters) – Fiat Chrysler Automobiles NV and the United Auto Workers (UAW) union on Saturday announced a tentative agreement for a four-year labor contract, a boost for the automaker as it works to merge with France’s Groupe PSA.

Italian-American Fiat Chrysler and PSA, the maker of Peugeot and Citroen, last month announced a planned $50 billion merger to create the world’s fourth-largest automaker.

The tentative agreement with Fiat Chrysler, which is subject to ratification by the union members, follows contracts that the UAW already concluded with Ford Motor Co and General Motors Co.

The deal with GM followed a 40-day strike in the United States that virtually shuttered GM’s North American operations and cost the automaker $3 billion.

The UAW on Saturday said the contract with Fiat Chrysler included a commitment from FCA to invest $9 billion, creating 7,900 new jobs over the course of the four-year contract. Of the $9 billion, $4.5 billion was announced earlier this year, to be invested in five plants and creating 6,500 jobs.

Detailed terms of the tentative agreement were not released, but they are expected to echo those under the new contracts with GM and Ford, as the UAW typically uses the first deal as a pattern for the others.

“FCA has been a great American success story thanks to the hard work of our members,” UAW acting President Rory Gamble said in a statement. “We have achieved substantial gains and job security provisions for the fastest growing auto company in the United States.”

Ratification is not a sure thing. Rank-and-file UAW members at FCA in 2015 rejected the first version of a contract. In addition, a lawsuit related to a federal corruption probe could also raise doubts among union members about the terms agreed.

The federal corruption led GM to file a racketeering lawsuit against FCA, alleging that its rival bribed union officials over many years to corrupt the bargaining process and gain advantages, costing GM billions of dollars. FCA has brushed off the lawsuit as groundless.

Under the UAW’s deal with GM, the automaker agreed to invest $9 billion in the United States, including $7.7 billion directly in its plants, and to create or retain 9,000 UAW jobs.

Ford’s contract included commitments to invest more than $6 billion in its U.S. plants and to create or retain more than 8,500 UAW jobs.

The deals with GM and Ford also created a pathway to full-time employment for temporary workers and left healthcare insurance coverage unchanged.

Both automakers also agreed to signing bonuses, with $9,000 for full-time Ford workers and $11,000 for workers at GM.

(Reporting by Nick Carey; Editing by Leslie Adler)

FILE PHOTO: FCA’s Manley and Elkann speaks at the North American International Auto Show in Detroit, Michigan

PURCHASE, N.Y., Nov. 21, 2019 (GLOBE NEWSWIRE) — Atlas Air Worldwide Holdings, Inc. (AAWW) today confirmed that its subsidiaries Atlas Air, Inc. and Southern Air, Inc. have prevailed in another legal dispute with the union that represents its pilots in ongoing negotiations, the International Brotherhood of Teamsters.

The decision by the U.S. Court of Appeals for the Second Circuit affirms a March 13, 2018, decision by the Southern District Court of New York compelling the Teamsters to arbitrate whether the merger provisions in Atlas Air and Southern Air’s collective bargaining agreements apply to the bargaining process. Today’s decision, as well as two binding decisions by arbitrators rendered in favor of both Atlas Air and Southern Air this summer, have made clear that IBT must engage in the current Atlas Air and Southern Air collective bargaining agreements’ expedited and defined process for achieving a joint collective bargaining agreement.

In a separate labor-related decision rendered in July 2019, the U.S. Court of Appeals for the District of Columbia unanimously affirmed a federal district court ruling in November 2017 that ordered the union to stop an intentional and illegal work slowdown by Atlas Air pilots in violation of the Railway Labor Act. The unanimous ruling from a three-judge panel upheld the lower-court order that blocked the union from continuing to engage in improper activities such as excessive sick calls on short notice or refusing to volunteer for open time.

“With these decisions behind us, it’s time for the union to honor its obligations under the collective bargaining agreements and these binding decisions. Specifically, the union has an obligation to produce an integrated seniority list and engage in direct bargaining for a defined and limited period of time. In ongoing negotiations, the union has yet to provide us with a comprehensive economic proposal covering pay and benefits for evaluation. We remain committed to working collaboratively with union leaders to efficiently negotiate and complete the contract,” said William J. Flynn, Chairman and Chief Executive Officer, Atlas Air Worldwide.

For more information about the contract negotiations process and updates, please visit AtlasAir5YPilots.com and follow @AtlasAir5Y on Twitter.

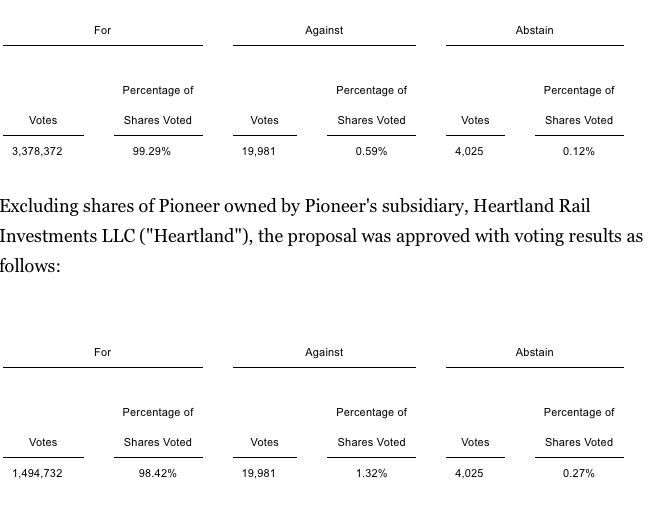

PEORIA, Ill., July 19, 2019 /PRNewswire/ — Pioneer Railcorp (OTC: PRRR, “Pioneer”), a railroad holding company that owns short-line railroads and several other railroad-related businesses including a railroad equipment company and a contract switching services company, today announced that its shareholders have approved the previously announced definitive merger agreement with BRX Transportation Holdings, LLC (“BRX”), an entity formed by Brookhaven Rail Partners (“Brookhaven”), Related Infrastructure (“Related”) and Stephens Capital Partners LLC (“Stephens”). The proposal to approve the merger agreement and the transactions contemplated thereby was approved with voting results as follows:

Under the terms of the merger agreement, BRX will acquire through merger all of the outstanding shares of Pioneer’s Class A common stock. Shareholders other than Heartland will receive $18.81 per share in cash and the Heartland shares will be cancelled without consideration.

Consummation of the merger remains subject to various closing conditions, including operating performance by Pioneer within a specified working capital floor and debt ceiling. Subject to satisfaction of the closing conditions, the transaction is expected to close in late July 2019. Upon closing of the transaction, Pioneer will become a wholly-owned subsidiary of BRX and its Class A common stock will cease trading on the OTC Markets.

Arnold & Porter is acting as legal advisor to BRX in this transaction. BMO Capital Markets is serving as exclusive financial advisor to Pioneer in connection with this transaction and Briggs and Morgan, P.A. is acting as Pioneer’s legal advisor.

About Pioneer Pioneer Railcorp is the parent company of 15 short-line common carrier railroad operations, an equipment leasing company, two service companies and a contract services switching company. Pioneer and its subsidiaries operate in the following states: Alabama, Arkansas, Georgia, Illinois, Indiana, Iowa, Kansas, Michigan, Mississippi, Ohio, Pennsylvania and Tennessee. For more information on Pioneer, please visit www.Pioneer-Railcorp.com

About Brookhaven Brookhaven Rail Partners is an affiliate of Denver-based Brookhaven Capital Partners, a privately held, real estate and infrastructure investment and management firm. Brookhaven and its principals have a 25-year track record of investing in, operating and developing critical transportation assets that support industry, and promote new economic development, community investment, and job creation. For more information on Brookhaven, please visit www.BrookhavenPartners.com